proposed estate tax law changes

The estate tax changes that were anticipated in the final months of 2021 are apparently not materializing leaving some people scratching their heads as to what they should do next. The tax reform proposals announced by the Administration in April and the General Explanations of the Administrations Fiscal Year 2022 Revenue Proposals published.

The Generation Skipping Transfer Tax A Quick Guide

Estates valued over 35 million but less than 10 million would be subject to an estate tax rate of 45.

. A persons gross taxable estate includes the value of all assets including even proceeds payable via life insurance policies. The current 2021 gift and estate tax exemption is 117 million for each US. For the vast majority of Americans the federal estate tax the death tax has been a non-issue since 2010 when the exemption was raised to 5 million and indexed for inflation.

The Biden Administration has proposed sweeping estate tax impacts to the estate and gift structure. The proposals are part of the so-called Budget bills promulgated by each group. This means the current inflation-adjusted exemption of 11700000 per person would be reduced to approximately 6000000.

PROPOSED ESTATE AND GIFT TAX LAW CHANGES OCTOBER 2021. Estate and Gift Tax Exemption Decreases Lower the gift tax and estate tax exemption from the current 117 million per person 234 million per married couple to the 2010 level of 5 million per person adjusted for inflation. The proposed law would reduce the federal gift and estate tax exemption from the current 10 million exemption indexed for inflation to 117 million for 2021 to 5 million indexed for inflation to roughly 62 million as of january 1 2022.

July 13 2021. Effective January 1 2022 the federal estate and gift tax exclusion will be cut in half to about 60 million after. This income tax treatment would continue under the proposed bill without any change from the current law.

Changes to the Charitable Income Tax Deduction. Starting January 1 2026 the exemption will return to 549 million adjusted for inflation. The For the 995 Percent Act proposes a sliding scale for rates as follows.

With inflation this may land somewhere around 6 million. The current lifetime exemption is 117 million dollars for an individual and 234 million for a. Estate gift and GST tax exemptions will remain at 117 million with increases allowed for inflation in 2022-2025.

Current law provides that the individual estate and gift tax exemption will be reduced to 5000000 adjusted upwards each year for inflation in 2026. The Biden campaign is proposing to reduce the estate tax exemption to 3500000 per person. The Biden Administration has proposed significant changes to the income tax system.

The Biden campaign proposed reducing the estate tax exemption to 35 million per person 7 million for a married couple which is what it was in 2009 while increasing the top rate to 45. Five proposed changes to the estate and gift tax laws may 5 2021 by. The BBBA would return the exemption to its pre-TCJA limit of 5 million in 2022.

That amount is annually adjusted for inflationfor 2021 its 117 million. It is important to emphasize that Governor Cuomo has not proposed an increase to New York State estate tax in his proposed Budget bill. Proposed Estate Tax Law Changes View Larger Image House and Senate Democrats are working with the Biden administration to pass legislation to fund their infrastructure initiatives including wide-ranging social programs and tax legislation to pay for those programs at least in part.

Grantor Trusts Grantor trusts trusts whose taxable activity and income are reported on the income tax returns of the persons who created the trusts have been a target of proposed legislation this year. The House Ways and Means Committee proposal accelerates this reduction lowering the exemption amount to 6020000 after the inflation adjustment effective as of January 1 2022. Proposed tax law changes in the draft legislation that could affect clients estate planning include.

Estate and Gift Tax Exclusion Amount. Estates valued over 10 million but less than 50 million would be subject to an estate tax rate of 50. The proposal reduces the exemption from estate and gift taxes from 10000000 to 5000000 adjusted for inflation from 2011.

Estate and Gift Tax Exclusion Amount. Estates valued over 50 million but less than 1 billion would be subject to an. Under the current proposal the estate.

Reduce the current 117 million federal ESTATE tax exemption to 35 million. If a decedent dies in 2026 with an estate of 11700000 the exemption amount would. The TCJA doubled the gift and estate tax exemption to 10 million through 2025.

The bill would dramatically reduce the federal estate and gift tax exclusion from its current level of 117 million. Under the current tax law the higher estate and gift tax exemption will Sunset on December 31 2025. The proposed law would reduce the federal gift and estate tax exemption from the current 10 million exemption indexed for inflation to.

Instead it contains three primary changes affecting estate and gift taxes. Proposals to decrease lifetime gifting allowance to as low as 1000000. Read on for five of the most significant proposed changes.

Under current law the existing 10 million exemption would revert back to the 5 million exemption amount on January 1 2026. The New York State Senate and Assembly have recently released proposals to change the New York State estate tax. The proposed impact will effectively increase estate and gift tax liability significantly.

Biden proposed reducing the federal estate tax exemption to 35 million per person 7 million for a married couple which was the exemption in. The proposed law would reduce the federal gift and estate tax exemption from the current 10 million exemption indexed for inflation to 117 million for 2021 to 5 million indexed for inflation to roughly 62 million as of January 1 2022. While there are no proposed changes to the charitable deduction for estate tax purposes and it remains to be seen how the proposed changes to the estate tax would impact charitable giving at.

Estate and gift tax exemption. The law would exempt the first 35 million dollars of an individuals gross taxable estate or 7 million for a married couple from estate tax. The exemption is the amount that each person is.

Thankfully under the current proposal the estate tax remains at a flat rate of 40.

Must Read New York City Real Estate Tax Changes Estate Tax Real Estate Tips Nyc Real Estate

Pin On Real Estate Tax Tips

March Madness Nfib Estate Tax March Madness Small Business

The Unspoken Cost Of Dying A Summary Of Philippine Taxes After Life Lexology

Biden S Tax Plan Would Raise Capital Gains And Eliminate Stepped Up Basis 042621 Raising Capital Capital Gain How To Plan

Pin By Tina On Irs In 2022 Irs Taxes Capital Gains Tax Tax Brackets

Philadelphia Estate And Tax Attorney Blog Irs Payment Plan Business Plan Template Free Irs

It May Be Time To Start Worrying About The Estate Tax The New York Times

China Income Tax Calculation Paying Taxes Teaching Jobs Income Tax

Legacy Assurance Plan Pointing About The Federal Estate Tax And How This Tax May Affect Larger Estate Planning Estate Planning Checklist Revocable Living Trust

How Do State Estate And Inheritance Taxes Work Tax Policy Center

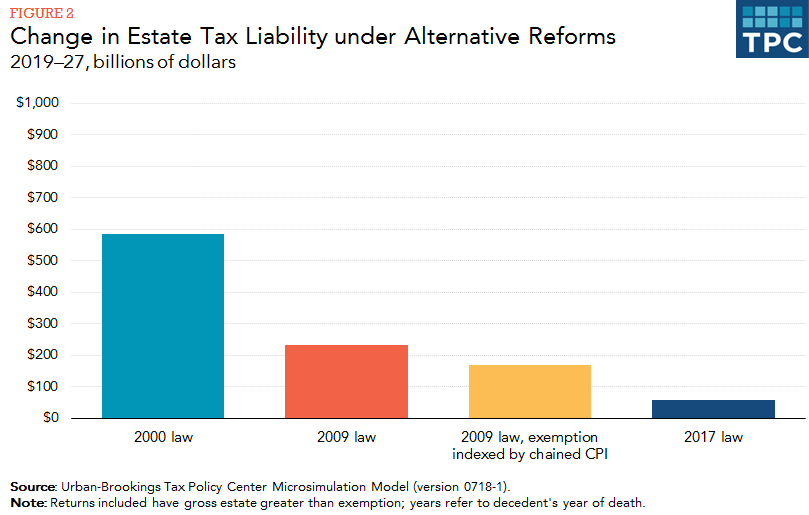

How Could We Reform The Estate Tax Tax Policy Center

The Generation Skipping Transfer Tax A Quick Guide

Great Changes In Inheritance Tax In Andalucia

This Is Such A Powerful Quote There S Nothing More Important Than Family Share This Post If You Agree Quoteofthe In 2022 Powerful Quotes Family Plan How To Plan

Pin By Saklaw Ph On Pending Bills And New Laws Estate Tax Train Package Reform

Gift Tax Exemption Lifetime Gift Tax Exemption The American College Of Trust And Estate Counsel

How Could We Reform The Estate Tax Tax Policy Center

Grantor Trust Estate Planning Strategies To Implement Before The Biden Tax Proposals Take Effect Advicers Grantor Trust Estate Tax Estate Planning